This tutorial guides you in recommending a grant on behalf of your client through our advisor platform, GivingCentral. If you have not already done so, you’ll need to register on GivingCentral.

1. Initiate the grant

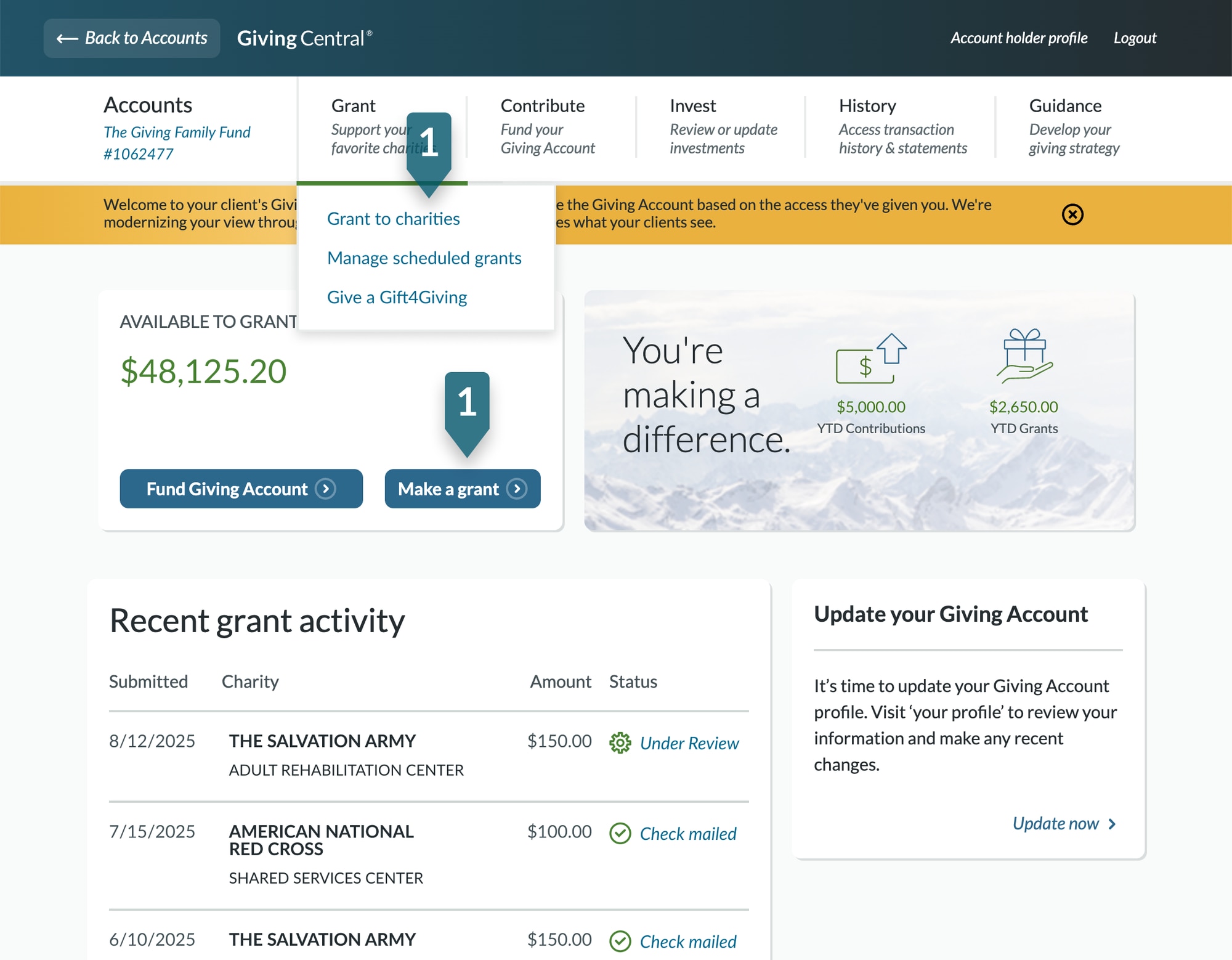

From your GivingCentral dashboard, scroll to Active Giving Account, the list of the Giving Account for which you have transactional access. Select the Giving Account your client intends to use to fund this grant recommendation.

On the Account Summary page, click the Make a Grant button or hover over the Grant menu tab and select Grant to charities. (If you do not see these options, you will need to request transactional access from your client.)

Add a new charity to the grant list

To recommend a grant to an organization, the charity must first be in the client’s grant list. You can either search for a new charity to add to the list or, if the client has supported this organization in the past, you can locate it within their charity list.

1. Add a new charity

Click on the “Find a charity” button to find organizations your client wants to support and proceed to the next page of the tutorial.

2. Find a charity your client has previously supported

If your client has previously supported the charity, you can find the organization in the client’s grant list. Type in the search bar above the list and customize the search timeframe with the “Viewing” dropdown to change the timeframe of the charity list. Click “Help” for further information anytime in the process.

Find the new charity your client wants to support

1. Search for a new organization

Use the search functionality to find a new charity your client would like to support. Our database includes over 1.8 million non-profit organizations. You can search by entering the charity name, address, or federal tax ID and then selecting “Search”.

2. Filter the search results

You can narrow your search by state if your client is looking for a local chapter of a larger national organization. You can also refine by sector. If the organization is not listed in the search results, you have the option to enter it manually, by clicking “Recommend a charity” at the bottom.

To learn more about a charity, view “Research Charity” with information from GuideStar®.

3. Add the charity to the grant list

Once the correct organization is found, click on the “Select” button to the right.

Validate the organization’s information is correct

Ensure the charity information is correct for the organization your client wants to support.

1. Validate the pre-populated nonprofit information

Click “Charity details” to review the organization’s legal name and mailing address and confirm it is the organization your client would like to support in the popup. The default information is provided by the IRS.

2. If preferred, add additional contact information

If desired or requested by your client, add a contact name and/or phone number for the organization. Save any changes.

Note, this additional information is not required and is used for routing purposes only. Payments are made to the order of the organization name only.

Tip: Make changes only if you are confident the legal mailing address has changed. Entering a new address for the organization requires additional due diligence and may delay processing of the grant recommendation.

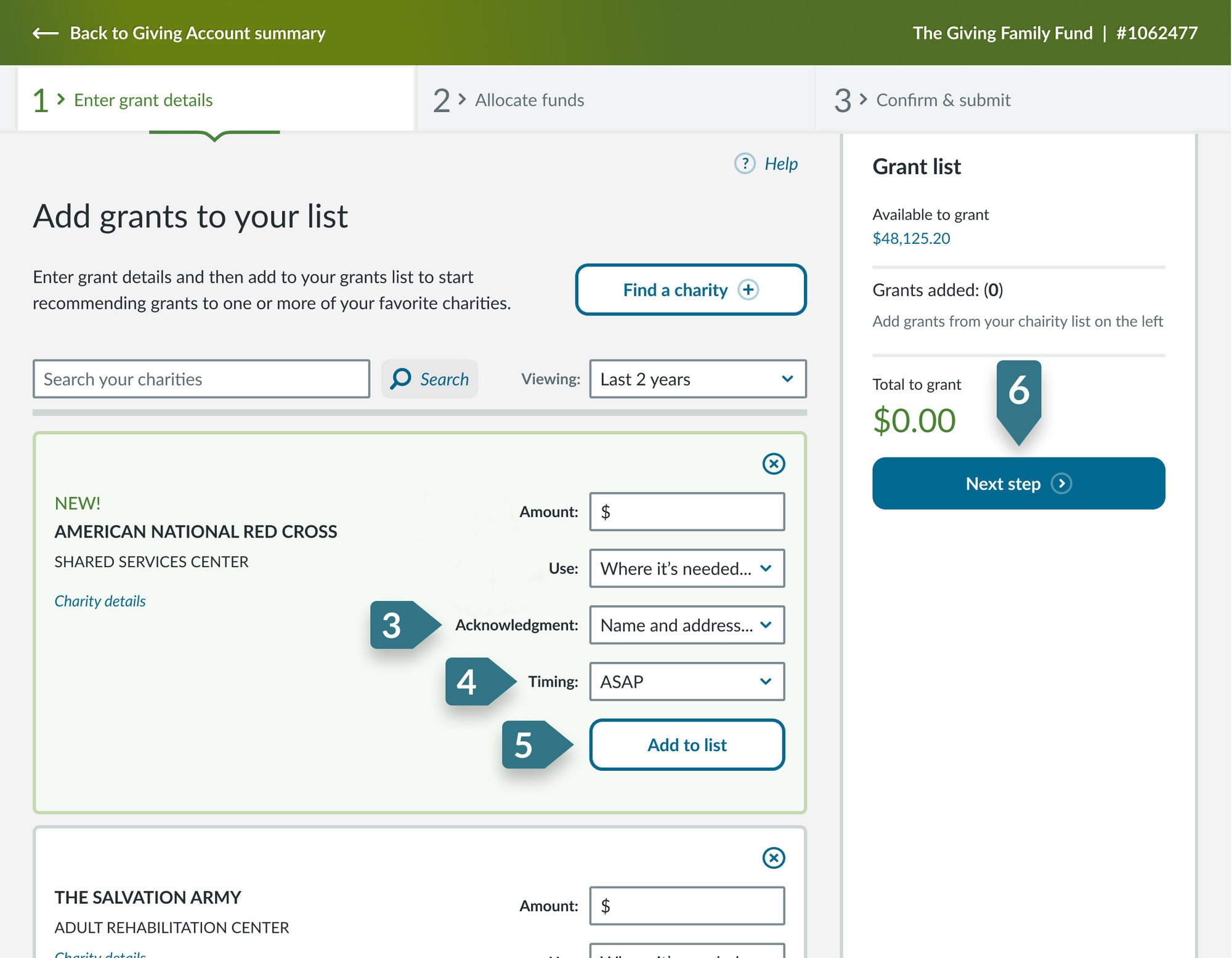

Specify the amount and how the grant should be used

The designation informs the organization how the funding is to be used.

1. Indicate the grant amount

Enter the grant recommendation dollar amount in the “Amount” box. If the client has a managed account or multiple accounts, indicate the source of the funds. If you need to change this later, there is an option to “Edit” after the grant is added.

IMPORTANT: The full Giving Account balance cannot be granted in GivingCentral. Please contact Fidelity Charitable for assistance if your client would like to grant the full balance.

2. Select the grant use

From the drop-down menu, select a category that tells the charity how your client would like the grant to be used. Certain fields will allow you to add more detail about the use. The default is “Where it’s needed most” which allows the organization to decide where the funds should be directed.

Tip: Ensure the purpose of the grant is permissible. While you can customize a designation or create your own, these recommendations require additional due diligence and may delay processing of the grant recommendation.

Specify the amount and how the grant should be used (cont.)

The designation informs the organization how the funding is to be used.

3. Indicate how your client should be acknowledged

Your client has several options for acknowledgement – their full name and mailing address, their Giving Account name only, or to remain anonymous. The “Edit” button allows you to verify your client’s address is correct.

4. Specify the grant timing

Select when your client would like funds to be distributed. You have three options for grant timing: submit a one-time grant as soon as possible, schedule a one-time grant for the future, or create a recurring grant. The default selection is a one-time grant issued “ASAP (as soon as possible).”

5. Add the grant to the grant list

If your client would like to make additional grant recommendations, you can repeat the previous steps to add multiple grants to the grant list.

6. When all grant details are complete, select “Next steps”.

Tip: Typical grant processing time is 2–10 business days. Plan accordingly if additional due diligence may be required.

Allocate funds from the Giving Account

If the funds in the client’s Giving Account are invested in more than one pool, you can identify which pools the grant recommendation should be funded from. If the client only has one investment pool or a managed account, you will not see this screen. You have two options for investment allocation:

1. Allocate per current percentages

Allows you to quickly allocate funds based on your current pool market values. Recommending the same allocations helps maintain the current investment strategy.

2. Specific allocations

Pool allocations can be entered in by a percentage or a dollar amount. Allocation cannot exceed the available pool market value.

3. Review total

The total must add up to 100%.

Tip: Check the status of a grant recommendation anytime in GivingCentral.

Confirm all details are correct and submit

The final summary page displays all details regarding the grant details and pool allocations from the previous steps. This is your opportunity to ensure all information is correct before you submit on behalf of your client.

1. Review and confirm all grant recommendation details and edit if necessary

You can view and edit grant details and charity details if you need to make changes before submitting the grant recommendation.

2. Add your certification

Once you have proceeded to the next step, you will be asked to agree to several certifications. You can submit the grant recommendation after agreeing to the statements.

3. Submit the grant

Click “Submit grant” to send the grant recommendation to Fidelity Charitable for processing.

Grant recommendation submitted

Congratulations, your client’s grant recommendation has been submitted to Fidelity Charitable for processing.

1. Review grant history

Access the details of your client’s grant recommendation at any time on the grant history page.

2. Print, if desired

Click the “Print” button to keep a hard copy for your records.

Nonprofits added to the donor's charity list are visible to everyone with transactional access on the Giving Account. The charity list can be searched or filtered by time period.

Fidelity Charitable asks for online grant recommendations for the convenience and security of our donors and advisors. Online grant recommendations save time, reduce errors, and allow submissions on any day or time—all with the enhanced protection of a secure login and multifactor authentication. Donors and advisors who need assistance with online granting can access our guide for how to recommend a grant online for the Giving Account (opens in new tab or window) for donors or GivingCentral for advisors.

Where can I find my “favorite” grant recommendations and/or repeat a grant recommendation in GivingCentral?

From your client Giving Account summary page, hover over “History” in the menu tab and then select “Grant history.” From the list, click on the grant ID or status link to view the full details. Once on the “Grant details” page, click the regrant button in the upper right-hand corner.

What are the things to keep in mind when recommending a grant?

You can recommend a grant to virtually any IRS-qualified 501(c)(3) public charity or private operating foundations on behalf of your client, although the client may not receive a "more than incidental benefit" in return (such as tickets to a charitable event).

The minimum grant is $50. In addition to the amount of a grant, you can also specify your client's desired use for the funds and how they would like to be acknowledged. These details will be sent to the charity along with the grant.

What is the best way for me to recommend a grant on behalf of my client?

To make a grant on behalf of your client through GivingCentral, you must have transactional access on the Giving Account. Account access can be requested during the account opening process or from the GivingCentral dashboard at any time once the Giving Account is established. Once access is approved by your client, use this tutorial to walk through recommending a grant step-by-step.

You can check the grant status for your client by logging in to GivingCentral and clicking on your client’s Giving Account name. From there, go to Recent Grant Activity on the dashboard. To view more, you can hover over the History menu tab and select “Grant history.”

Your client can check the status of a grant by logging in to the donor portal, hovering over the History menu tab, selecting “Grant history,” and clicking the grant ID to view the full details, including the status.

To protect the integrity of the program, and to ensure that we are following the rules outlined by the IRS for registered 501(c)(3) programs, we not only go through a process of verifying the charity but also the type of Grant being made to ensure that it qualifies. More information can be found here.

Can a grant from my client's Giving Account be recommended for the tax-deductible part of a ticket to a charitable event?

No. Bifurcated or "split" gifts cannot be made from the donor-advised fund. For example, grants intended to pay all or a portion of the cost of tickets to attend a charitable event will not be made. This includes grants for the charitable, or tax-deductible, portion of the ticket price. The FULL ticket price (the tax deductible AND non-tax deductible portions) must be paid out of pocket and separate from any Fidelity Charitable grants.

What about recommending a grant for a sponsorship?

Here’s an example: Rebecca would like to attend the Annual Gala at her favorite charity. The charity offers individual tickets priced at $500 ($250 tax-deductible) or a Patron Sponsorship for $10,000 that comes with 10 tickets for seats at a premium table ($7,500 tax-deductible). Rebecca would like to use all 10 seats so her friends and family can attend the gala with her. For Rebecca to be within Fidelity Charitable policy, she would have to pay the full minimum ticket price of $500 for each attendee, totaling $5,000.

She can recommend a grant for the remaining $5,000 from her Giving Account at Fidelity Charitable as long as this amount is considered fully tax-deductible with no goods or services being provided in connection to the grant.

Fidelity Charitable’s policies are in compliance with the Pension Protection Act of 2006 (PPA) which enacted certain laws applicable to donor-advised funds, including excise taxes on prohibited benefits under IRC section 4967.

In December 2017, the IRS released Notice 2017-73 that requested comments on potential regulations the IRS is considering with respect to donor-advised funds. The rules proposed in the Notice are largely consistent with Fidelity Charitable’s policies and procedures.

What does the term “more than incidental benefit” mean?

Grants must be recommended exclusively for charitable purposes with no more than incidental benefits to an Account Holder or related third party. A “more than incidental” benefit generally includes items with financial value, such as includes tickets to attend an event, raffle tickets, auction items, or the provision of any other goods or services. Certain items of minimal value are considered an “incidental benefit” such as logo-bearing keychains, coffee mugs, or calendars.