Charitable lead trusts

Efficiently transfer assets to family members, reduce tax liability and make a charitable impact

A charitable lead trust is an irrevocable trust designed to provide financial support to one or more charities for a period of time, with the remaining assets eventually going to family members or other beneficiaries.

Charitable lead trusts are often considered to be the inverse of a charitable remainder trust. Charitable lead trusts operate for a set term, which could be the life of one or more individuals, and payments are made to one or more designated charitable beneficiaries for that time period. After the end of the trust term, the remainder of the trust is distributed to non-charitable beneficiaries—such as family members. A charitable remainder trust, in contrast, can provide a stream of income for family members for the term of the trust before the remaining assets are transferred to one or more charitable organization beneficiaries.

A charitable lead trust can be funded either during the lifetime of the individual creating the trust or by will. It is a strategy most frequently used by the charitably inclined for estate or gift tax planning purposes. It can potentially provide benefits such as an income tax deductions or estate or gift tax savings on assets ultimately passed to the individuals designated as remainder beneficiaries. At the same time, the trust distributes regular payments to benefit a preferred charity or charities during the term of the trust.

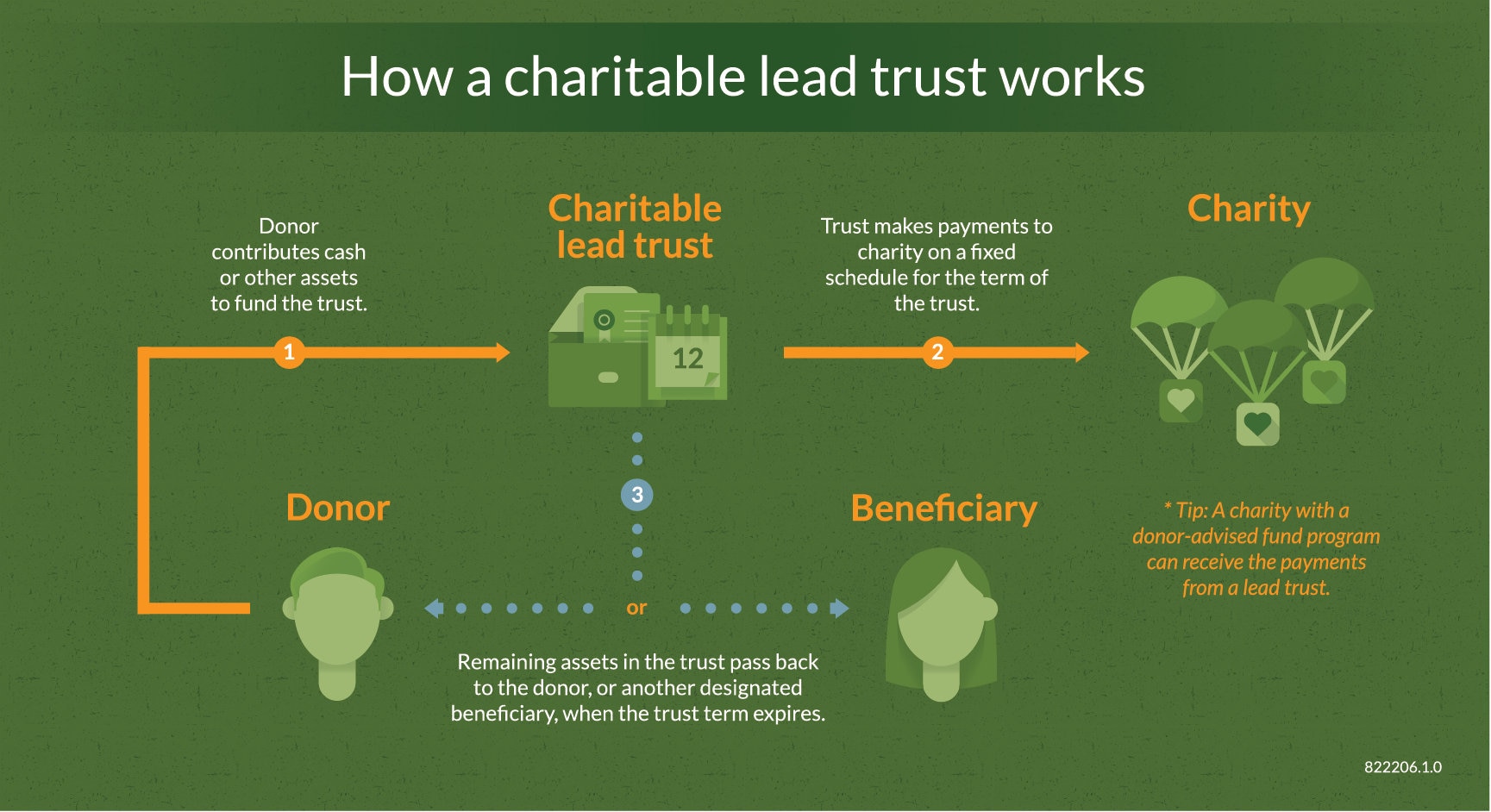

How a charitable lead trust works

At their most basic level, a charitable lead trust works in the following way: The grantor, or person establishing the charitable lead trust, makes a contribution to fund the trust which is set up to operate for a fixed term such as a set number of years or the life of one or more people. Payments from the trust are disbursed to the selected charity or charities as either a fixed annuity payment or a percentage of the trust, depending on how the trust has been structured. Finally, at the end of the term, the remaining assets are distributed to non-charitable beneficiaries, often family members. Charitable trusts are usually complicated and subject to specific IRS rules, so anyone considering establishing a charitable trust, including a charitable lead trust, should consult with their legal or tax advisor.

1. Make a contribution to fund the trust. Depending on the type of charitable lead trust you select, you may be eligible to take an immediate partial tax deduction with cash contributions. The calculation of the income tax deduction takes into consideration the term of the trust, the projected lead payments, and IRS interest rate that is used to assume a certain rate of growth of trust assets.

Certain assets such as publicly traded stock, real estate, private business interests and private company stock could also be contributed, but come with added considerations about tax treatment and to may need to be sold to ensure enough revenue to fund the trust payments.

2. Payments are sent to the charity. The charitable lead trust provides payments on at least an annual basis to at least one qualified charitable organization for a fixed number of years, the lifespan of one or more individuals, or a combination of the two. Unlike charitable remainder trusts, charitable lead trusts are not held to the same mandatory time limit of 20 years if you select the fixed term option. Also, there is no required minimum or maximum payment to the charitable beneficiaries, so long as payments are made at least annually.

3. After the specified trust term, the remaining charitable lead trust assets are distributed to the designated non-charitable beneficiaries. Once the term of the charitable lead trust ends, the principal is distributed to you or the other designated beneficiaries in a manner that can minimize or even eliminate transfer taxes.

The word “lead” in charitable lead trust refers to a “lead interest” in the trust, which is the charity’s right to receive payments for the trust for the specified term. If established as a charitable lead annuity trust, the charity will receive a specified amount from the trust each year that typically remains the same from year to year. If established as a charitable lead unitrust, the charity will have the right to receive a specified percentage of the trust assets each year, and the precise amount of the payment to the charity can vary from year to year accordingly. The choice of annuity vs. unitrust payments may have implications for the value of the remaining assets at the end of the trust term.

There are two overall types of charitable lead trust that affect its tax treatment—grantor and non-grantor trusts. Tax planning and other goals of the individual establishing the trust should guide the choice between these categories, as each provides distinct advantages and possible drawbacks.

- Grantor charitable lead trust: In a grantor charitable lead trust, the grantor can take an immediate income tax charitable deduction for the present value of the future payments that will be made to the charitable beneficiary, subject to applicable deduction limitations depending on whether the beneficiary is a public charity or a private foundation. However, this benefit should be considered in conjunction with the fact that the trust's investment income is taxable to the grantor during the trust's term.

- Non-grantor charitable lead trust: With non-grantor charitable lead trust, the trust—and not the grantor—is considered the owner of the trust assets. Accordingly, the grantor is not eligible to take an income tax deduction for the present value of the lead interest to charity. It is the trust itself that pays tax on its undistributed net income, and the trust is able to claim an unlimited income tax charitable deduction for its distributions to the charitable beneficiary. However, this trust structure offers greater benefits for transfer tax purposes.

Notably, both grantor and non-grantor trusts can be structured to be “reversionary,” meaning that the remainder assets revert to the individual(s) establishing the trust or “non-reversionary,” meaning that the remainder assets will be distributed to a beneficiary other than the originators. These choices will have additional impact on tax treatment.

Pair a charitable lead trust with a donor-advised fund to maximize your giving

Depending on the type of charitable lead trust established, changing charitable beneficiaries may be difficult or impermissible. Many donors wish to preserve a greater level of flexibility without having to amend the trust in the event of a desired change in charitable organizations. A donor-advised fund is a dedicated account for the sole purpose of supporting charitable organizations you care about. If you name a charity sponsoring a donor-advised fund program as the lead beneficiary of a charitable lead trust, you can retain greater flexibility over which charities ultimately benefit. How it works: the donor-advised fund will receive payments from the trust. Then, you can recommend grants from the donor-advised fund balance to support the charities of your choice. At the same time, you retain the benefits of the charitable lead trust in passing assets to your loved ones.

What assets may be contributed to a charitable lead trust?

You can use the following types of assets to fund a charitable lead trust:

- Cash

- Publicly traded securities*

- Some types of closely held stock*

- Real estate*

- Certain other complex assets*

* Assets may need to be sold or coupled with a cash donation to ensure the trust has adequate resources to disburse the required payments. There may also be tax consequences.

Considerations

- Unlike a charitable remainder trust, a charitable lead trust is not tax-exempt. Trust income is taxed like the income of any other complex or grantor trust.

- Requires legal setup and likely ongoing maintenance costs.

- Careful planning is required to ensure the trust can make its required payments during the trust term.

- The trust is irrevocable.

Key benefits:

- Reducing estate taxes. In the case of a non-grantor trust where trust assets pass to heirs, the property contributed to the trust will be considered part of the donor’s estate, but the donor’s estate will be eligible for an estate tax charitable deduction for the value of the interest paid to the charity. This may not only reduce the amount of tax your estate has to pay upon your death, but it may also preserve wealth for your heirs."

- Reducing gift taxes. If you make a contribution to a non-grantor charitable lead trust during your lifetime, you may be eligible for a gift tax charitable deduction, based on the present value of the interest going to the charity. However, if the remainder beneficiary of a charitable lead trust is someone other than yourself, then you might be subject to gift tax on the value of the remainder interest. It’s important to note, however, that it may be possible to structure the specific terms of the trust, such as length of term and payout percentage, in a way that could potentially eliminate gift taxes on the remainder amount passing to the end beneficiary.

Is a charitable lead trust right for me?

Anyone considering a trust will want to compare the benefits of various options for charitable giving. A non-grantor charitable lead trust could be good option if you want to pass appreciated assets to heirs and potentially reduce gift or estate tax consequences. However, since you lose access to those assets and any income they may generate for the trust term, you must be in a position to make that tradeoff.

A grantor charitable lead trust will offer a current tax deduction, though that may be offset by the fact that income on the trust will be taxable to the donor during the trust term.

As always, if you’re considering making charitable giving part of your estate plan, consult with your tax and estate planning advisor to determine the best vehicle and strategy for your situation. In fact, it’s important to communicate about these charitable giving vehicles not only with the financial professionals that support you, but also with your family.

How Fidelity Charitable can help

Since 1991, we have been helping donors like you support their favorite charities in smarter ways. We can help you explore the different charitable vehicles available and explain how you can complement and maximize your current giving strategy with a donor-advised fund. Join more than 395,000 donors who choose Fidelity Charitable to make their giving simple and more effective.

Ready to get started?

Opening a Giving Account is fast and easy, and there is no minimum initial contribution.

Or call us at 800-262-6039