What is a charitable gift annuity?

A contract that provides the donor a fixed income stream for life in exchange for a sizeable donation to a charity.

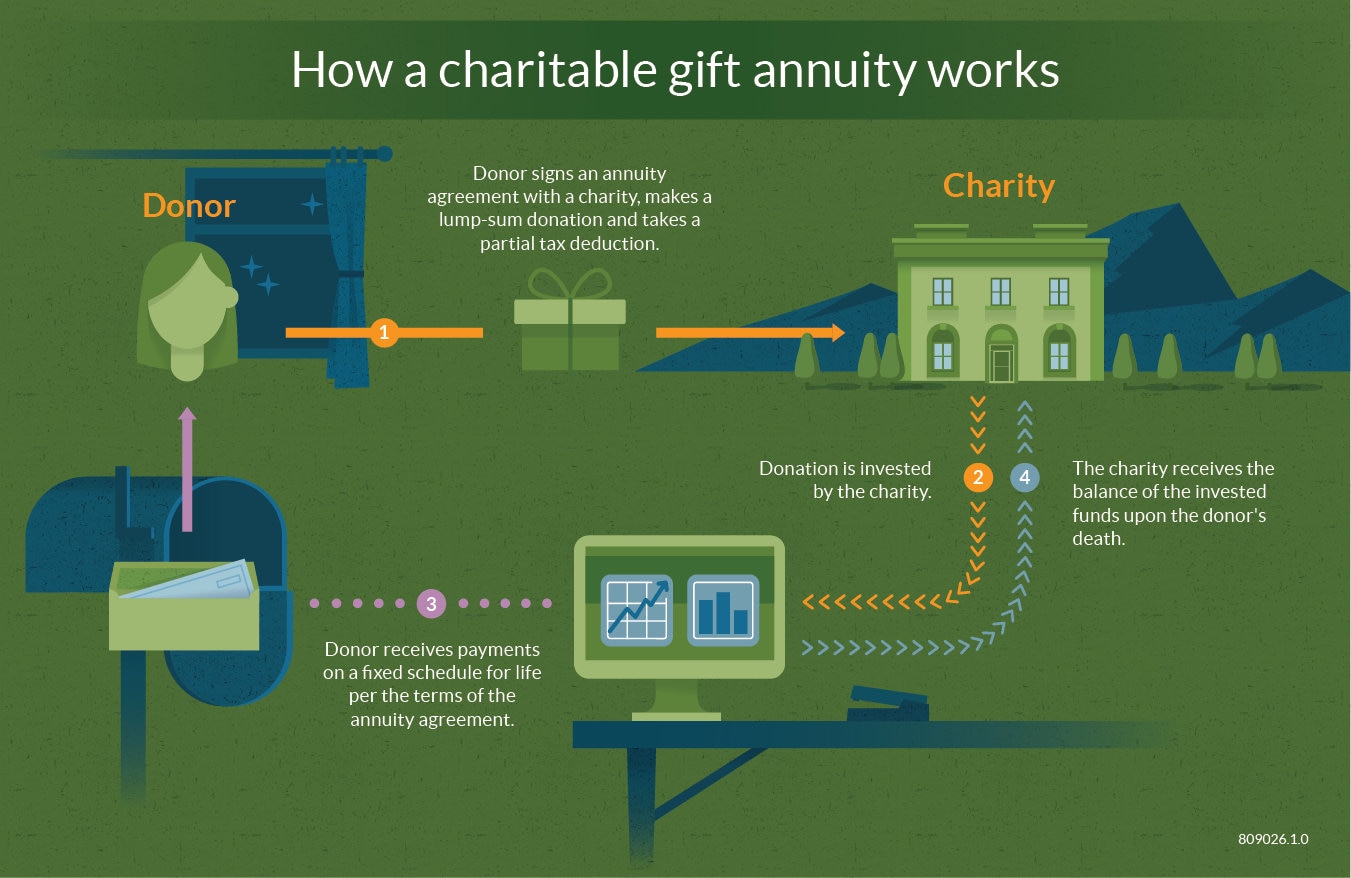

A charitable gift annuity is a contract between a donor and a charity with the following terms: As a donor, you make a sizable gift to charity using cash, securities or possibly other assets. In return, you become eligible to take a partial tax deduction for your donation, plus you receive a fixed stream of income from the charity for the rest of your life.

How does a charitable gift annuity work?

Many large nonprofit organizations, including a number of universities, offer charitable gift annuities. First, you make a donation to a single charity. Then, the gift is set aside in a reserve account and invested. Based on your age(s) at the time of the gift, you receive a fixed monthly or quarterly payout (typically supported by the investment account) for the rest of your life. At the end of your life (as well as your spouse’s, if you’re giving as a couple), the charity receives the remainder of the gift.

Individuals or couples can set up a charitable gift annuity. (You are the “annuitants,” which is the specific name for beneficiaries of annuities and many insurance policies.) Depending on the charity, your annuity can be funded with cash donations, but potentially also securities and gifts of personal property. Minimum gifts for establishing a charitable gift annuity may be as low as $5,000, but are often much larger.

In addition to the income stream, annuitants may also be eligible to take a tax deduction at the time of the original gift, based on the estimated amount that will eventually go to the charity after all the annuity payments have been made. A portion of the payments you receive may also be tax-free for a period of time based on your statistical life expectancy.

What is a gift annuity agreement?

A gift annuity agreement is a lifelong contract, not a trust, between a single nonprofit organization and an individual or couple, who are referred to as annuitant(s). The terms of this agreement will lock in the rate, amount and timing of all payments the annuitant(s) receive. The fundraising or planned giving department of the nonprofit you are interested in supporting will be able to provide information about whether it offers charitable gift annuities and at what rate; the fundraising or planned giving departments are typically the point of contact.

Because a gift annuity agreement is a contract with a single charity, there is no way to establish a charitable gift annuity that can support multiple charities at the same time.

Charitable gift annuity payments

Charitable gift annuity donors (annuitants) receive payments for the rest of their lives. The size of your payment is determined by many factors, including your age(s) when you set up the charitable gift annuity. (For example, younger donors will typically receive more payments but they’ll be smaller.) The amount is fixed and will never fluctuate or adjust for inflation. But it’s also guaranteed, backed by the charity’s entire assets, not just your gift, and will continue for the lives of the donors no matter how well or poorly the investments of the annuity perform.

Taxes

You may be eligible to claim a partial charitable tax deduction for the year in which you set up the charitable gift annuity. Why only a partial deduction? The IRS views one portion of your contribution as a gift, to be used immediately by the charity for its tax-deductible charitable purposes. The other portion is viewed as an investment for you, which ultimately generates your payments.

A second tax benefit may come by donating long-term appreciated stock or other property if the charity is able to accept these assets in place of cash. By donating non-cash assets directly, it is possible to reduce or eliminate the capital gains tax you’d ultimately pay if you sold them first and then donated the proceeds. This capital gains tax benefit is not exclusive to establishing a charitable gift annuity; it also applies when you gift long-term appreciated securities or personal property to any public charity that’s equipped to accept them, including Fidelity Charitable.

However, there is a potential tax drawback of a charitable gift annuity: part of your annuity income is taxable at the federal level, and possibly at the state level as well, depending on whether the state you live in has an income tax. The rules can be complex, so consider discussing the specifics of your situation with a tax advisor.

Annuity rates

Charitable gift annuity rates vary from charity to charity and are based on several factors, including the amount of the gift, as well as the donor’s age(s) at the time of the gift. Younger donors may often see significantly lower rates based on the longer expected term.

For illustrative purposes, a 60-year-old who donates $10,000 may receive a rate of 4.4% (paying $440 annually) while an 85-year-old will see a rate of 7.8% (paying $780 annually) for the same gift. Some charities offer higher rates for donors who agree to wait a number of years before starting to receive payments.

Compared to a traditional, non-charitable annuity, though, rates of return may be lower because the primary purpose of a charitable gift annuity is to benefit the charity. This is a consideration for anyone thinking about how to best balance their charitable goals with their financial plans.

Benefits of a charitable gift annuity

- Income stream for the rest of your life

- Immediate (partial) tax deduction, based on your life expectancy and the anticipated income stream

- Potential for a portion of the income stream to be tax-free

- Possibility of donating many types of assets: cash, securities plus personal property

- Reduced or eliminated capital gains tax liability for gifts of appreciated securities and personal property

- Supporting an organization you care about

Potential drawbacks

- Parting irrevocably with funds donated to create the annuity

- Subject to income tax on the income stream (payments from the annuity)

- Payments are fixed and won’t be adjusted for inflation

- Payments may be lower than with a non-charitable annuity because the primary purpose is for nonprofit support

- Cannot be used to support multiple charities unless you set up multiple annuities

Compared to a Charitable Remainder Trust

Another way to support a charity while collecting a steady stream of income is to establish a charitable remainder trust or CRT. A CRT works in a similar way to an annuity with a few key differences: You make a large donation to an irrevocable charitable trust. Depending on how it’s set up, you (or any beneficiary you name) receive a set percentage of the trust’s value on a specified basis, for example, 5% annually. After a predetermined time frame or the death of the last known beneficiary, any remaining CRT assets are distributed to the charity or charities of your choice. Adding another strategic layer, a donor-advised fund may be named a beneficiary of a CRT, easily allowing the support of multiple charities or a charitable legacy for heirs.

Charitable remainder trusts will likely require a greater minimum contribution to establish than a charitable gift annuity, typically $250,000, but also offer other benefits. Read more about charitable remainder trusts.

Other considerations for selecting a giving vehicle

Anyone considering their options for charitable giving will want to consider them in the context of an overall wealth or financial plan. With the goal of making a difference for a chosen charity or charities as a given, are other factors key to the decision? For example, is an income stream more valuable than a current tax deduction for your situation—or are both needs equally important to address? Donors will also want to consider how any vehicle they may select might impact their estate plans.

With this in mind, donors are wise to explore the full range of charitable vehicles to choose the method or combination of methods that best serves their charitable and financial goals. For example, a donor-advised fund, which is a dedicated account at a charity that exists for the sole purpose of supporting charitable organizations, will not generate an income stream. But it may be a better way to claim a full current tax deduction or take advantage of the full tax benefits of donating appreciated securities or non-publicly traded assets, compared to a charitable gift annuity. Plus, there’s the added benefit of supporting multiple charities at once.

A wealth advisor or other advisors specializing in tax and estate planning will be able to provide advice specific to your priorities and can be a valuable source of information in making the right choice for your situation.

How Fidelity Charitable can help

Since 1991, we have been helping donors like you support their favorite charities in smarter ways. We can help you explore the different charitable vehicles available and explain how you can complement and maximize your current giving strategy with a donor-advised fund. Join more than 395,000 donors who choose Fidelity Charitable to make their giving simple and more effective.

Ready to get started?

Opening a Giving Account is fast and easy, and there is no minimum initial contribution.

Or call us at 800-262-6039