Why donating restricted and control stock directly to charity can create a larger gift

Instead of selling restricted or control stock1 and donating the proceeds, it can be more efficient to donate the stock directly to a public charity.2 This simple change generally results in three significant benefits, for you and for the charity:

And there’s one more benefit of donating restricted or control stock to a public charity with a donor-advised fund program such as Fidelity Charitable: the opportunity to recommend investments that can grow tax-free within the Giving Account, potentially increasing the amount of charitable support over time.

Equity Compensation and Charitable Opportunities

Learn how equity-based compensation awards can be a smart way to fund your charitable giving. (02:51)

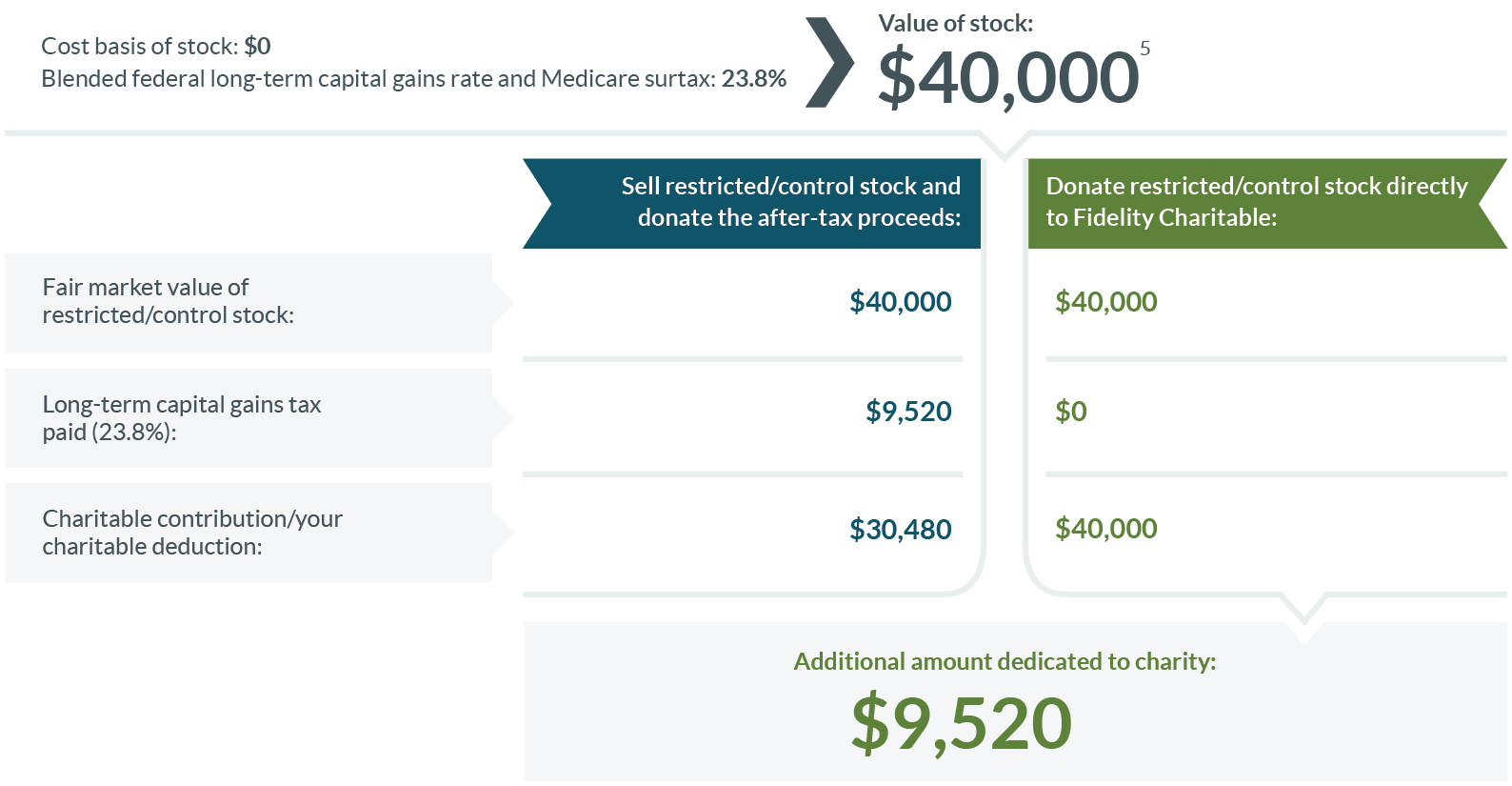

When you contribute restricted or control stock to Fidelity Charitable as opposed to selling the stock and donating the cash proceeds, your tax deduction and your charitable gift may increase by up to 23.8%. Consider this example:

What could this extra funding mean for charity? Depending on the organizations you choose to support, your contribution could look like this…

Drilling five wells in a third world country, providing thousands of people with fresh drinking water6

Creating local jobs through a well maintenance training program7

Luke has a concentrated and restricted position in company stock and is concerned about protection against tax exposure in his portfolio. He’s philanthropically inclined but doesn’t know how he wants to give, and doesn’t have a long-term charitable plan. Clean water is a cause he wants to support but the charities he knows don’t have the resources or experience to accept or efficiently liquidate restricted stock.

TIP: By contributing long-term appreciated restricted stock directly to a donor-advised fund at a public charity, you are generally entitled to a deduction of up to 30% of adjusted gross income (AGI), potentially allowing for a greater tax benefit and larger charitable gift than contributions of stock to private foundations, which are generally deductible at only 20% of AGI.

After speaking with his financial advisor, Luke chooses to establish a Giving Account at Fidelity Charitable. He contributes long-term appreciated restricted stock and Fidelity Charitable works with the company’s transfer agent, as well as its general counsel or compliance officer, to remove the restrictive legend. Fidelity Charitable then sells the stock and the Giving Account is funded with the proceeds. Luke is generally entitled to a tax deduction in an amount equal to the fair market value of the stock on the date of the contribution. Please note that donors should work with their tax advisors, as a qualified appraisal may be required to substantiate the fair market value of the gift.

By contributing the stock to Fidelity Charitable rather than selling, then donating the after-tax proceeds, Luke eliminates capital gains taxes on the sale of the stock. Plus, due to the flexibility of the donor-advised fund, the proceeds from the sale of restricted stock can be used to support multiple charities, all at once or over time. Now Luke can recommend grants to fund clean water programs at qualified charities, recommend investments for the remainder of the funds in his Giving Account for potential tax-free growth, and research more charities to support over time.

Potential benefits of giving restricted and control stock directly to Fidelity Charitable:

This hypothetical case study is provided for illustrative purposes only. It does not represent an actual donor, but is meant to provide an example of how a donor-advised fund can help individuals give significantly more for the causes they care about.

1This article addresses contributions of shares in a reporting issue whose shares are traded on an exchange.

2This assumes the stock has been vested, fully paid for and held for more than one year.

3This assumes the donor is itemizing. Thirty percent AGI limit. Other limitations on itemized deductions may apply.

4This assumes all realized gains are subject to the maximum federal long-term capital gains tax rate of 20% and the Medicare surtax of 3.8%, and that the donor originally planned to sell the stock and contribute the net proceeds (less the capital gains tax and Medicare surtax) to charity.

5Amount of the proposed donation is the fair market value of the restricted stock held more than one year that you are considering to donate.

6Assuming average costs of a well at $8,000, per Water Wells for Africa.

7Per The Water Project, Inc., a 501(c)(3) non-profit organization

Ready to get started?

Opening a Giving Account is fast and easy, and there is no minimum initial contribution.

Or call us at 800-262-6039